GURUGRAM, IN / ACCESS Newswire / June 3, 2026 / For millions of salaried Indians, there is no single “loan problem.” There are three: a credit card outstanding dues stacking up on one side, a personal loan EMI on the other, and a WhatsApp message from a recovery agent sitting unread in the middle. Reserve Bank of India data puts gross NPAs (loans marked bad by banks) in the retail segment at roughly ₹2.5 lakh crore. Behind that number are real people: employed, earning, but running out of road. The options exist. The question is which one fits.

Why Doing Nothing Is the Worst Choice

Ignoring all of this does not make it smaller. A missed EMI adds a late fee. A late fee becomes a penalty. A penalty compounds at 24-36% annually on credit cards, and most borrowers do not realize this until the balance has doubled. Each missed payment also chips away at the CIBIL score (the credit score used by Indian banks and NBFCs to evaluate loan applicants), which limits options exactly when more options are needed. Until recently, India had no organized framework for individual debt relief. Borrowers either negotiated alone, took another loan to cover the first, or quietly stopped picking up calls. Structured alternatives now exist, and using them early is significantly cheaper than waiting.

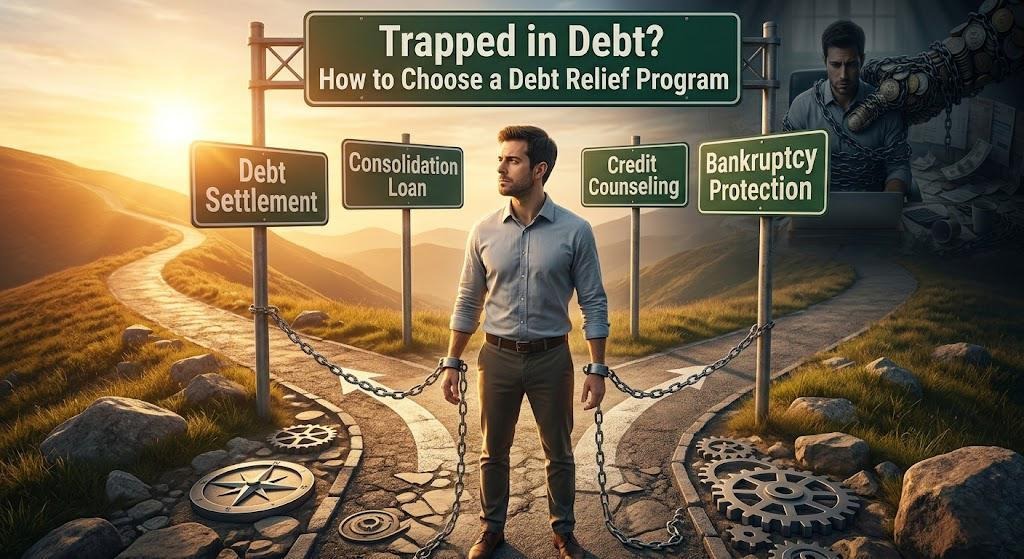

The Three Main Debt Relief Programs Explained

That is where structured debt relief comes in. Three programs exist in India today, and they are not interchangeable. Which one applies depends entirely on where a borrower currently stands in the repayment cycle, not on the size of the outstanding amount.

Loan Settlement

Settlement is not something a borrower chooses out of preference. Banks and financial companies only consider it when a borrower is in genuine financial difficulty and is truly unable to repay the full amount. It is a last resort, not a shortcut.

In a loan settlement, the bank agrees to accept a lump-sum amount lower than the total outstanding, marks the loan as “Settled,” and closes the matter. The CIBIL score takes a hit and the “Settled” tag stays on the credit report for up to 7 years. But for someone who is already defaulting and facing daily recovery calls, settlement can resolve the account and stop the damage from compounding further.

The anchor for this option is loan settlement, understanding the process, the CIBIL consequences, and what to realistically expect from the bank before starting any conversation.

Debt Consolidation Program

A debt consolidation program is for borrowers who are still paying, but barely. Three EMIs across three due dates, three different banks, three different interest rates, and often one of those rates is 36%+ on a credit card. Consolidation merges all of them into a single monthly payment at a lower interest rate. The borrower pays less each month, pays one amount to one account, and stops juggling due dates. This does not require any default. It is available to borrowers who are current on payments but stretched thin.

Debt Counselling

Counselling is the right first step for borrowers who are not sure where they stand. A certified debt counselor will look at total income, total outstanding debt, and all EMIs and tell the borrower honestly which program they qualify for and which makes financial sense. This costs nothing with reputable platforms and removes the guesswork before any commitment is made.

Not sure where to start? Speak with a certified debt counselor from a reputable debt relief company before committing to any program.

How to Choose the Right One

Understanding which of the three programs applies is easier than it looks. The decision comes down to one question: are payments still being made?

If yes, but the burden is getting unsustainable, debt consolidation is the right starting point. One EMI, lower rate, no default required.

If EMI payments have already stopped and recovery calls have started, loan settlement is worth exploring. Not as a quick exit, but as a structured resolution when repaying in full is genuinely no longer possible.

If the borrower is somewhere in between, not yet defaulting but not sure how long that will hold, counsel first. It takes 30 minutes and produces a clear answer.

Why FREED Is the Right Platform to Start With

Whichever program applies, the quality of the platform that delivers it matters as much as the program itself. FREED, India’s first comprehensive debt relief platform, was founded in 2020 and has since counselled over 2,000,000 borrowers, settled 20,000+ accounts, and has more than ₹3,200 Cr in enrolled debt under management. The founding team brings experience from the US debt settlement industry, where they managed over $2 billion in client debt before building an India-specific model.

The platform is backed by institutional capital from Aavishkaar Capital, Sorin Investments, and Piper Serica, investors focused on long-term, consumer-oriented financial services, not short-cycle fintech bets.

What separates FREED’s model is its structure. Monthly savings from enrolled borrowers go into a Special Purpose Account managed by India’s leading trusteeship firm. This is not an informal arrangement. The money is ringfenced, tracked, and used exclusively for settlement. Borrowers are not handing over cash to a middleman..

For borrowers facing recovery harassment during the settlement process, FREED has a dedicated tool called FREED Shield. It helps clients understand their rights under RBI guidelines, manage recovery agent contact, and where needed, draft a formal complaint to the bank or regulator. Borrowers in this situation do not have to navigate it without support.

FREED charges fees only on successful settlement. No upfront cost. No fee until the account is actually resolved.

Closing

The worst decision here is no decision. Debt compounds. CIBIL scores fall. Recovery pressure builds. None of these reverses on their own.

The borrowers who come out on the other side are not the ones who found a shortcut. They are the ones who assessed the situation clearly, matched it to the right program, and moved before the damage became permanent. Visit freed.care for a free consultation with a certified counsellor, no commitment, no cost, no pressure.

Contact:

Company Name: Freed India Private Limited

Contact : 0124-6663666

E-mail : info@freed.care

Website: https://freed.care/

SOURCE: FREED

View the original press release on ACCESS Newswire